(1).webp)

.webp)

.jpg)

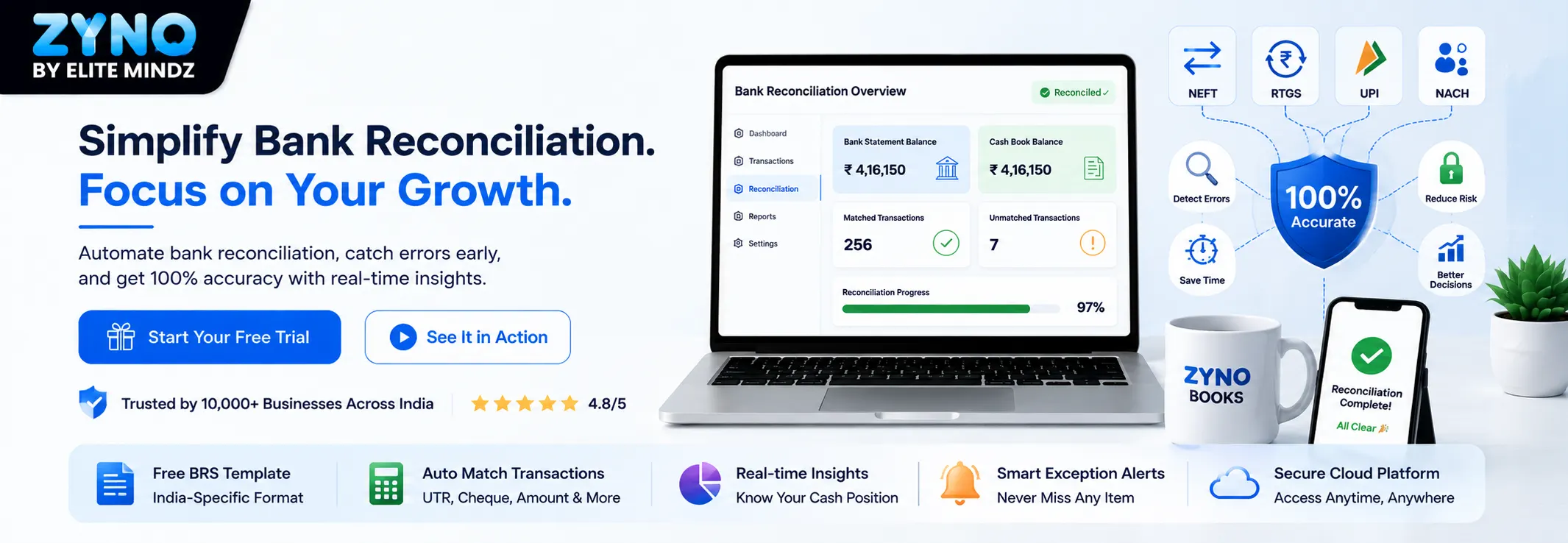

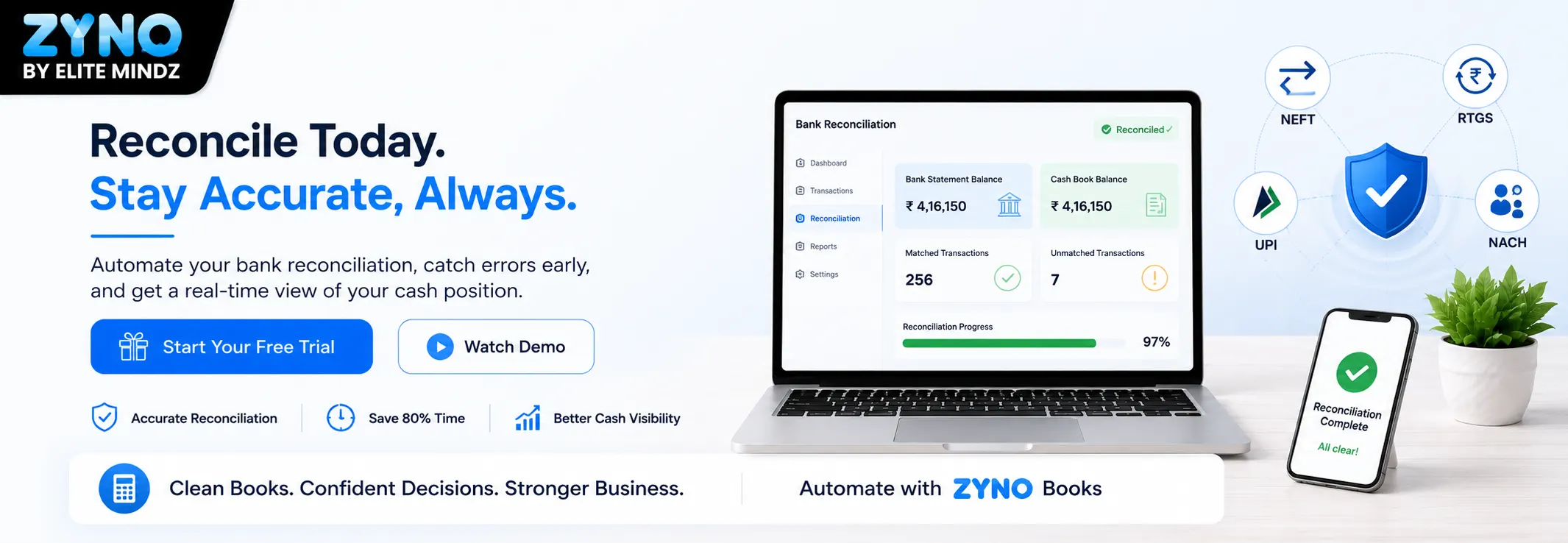

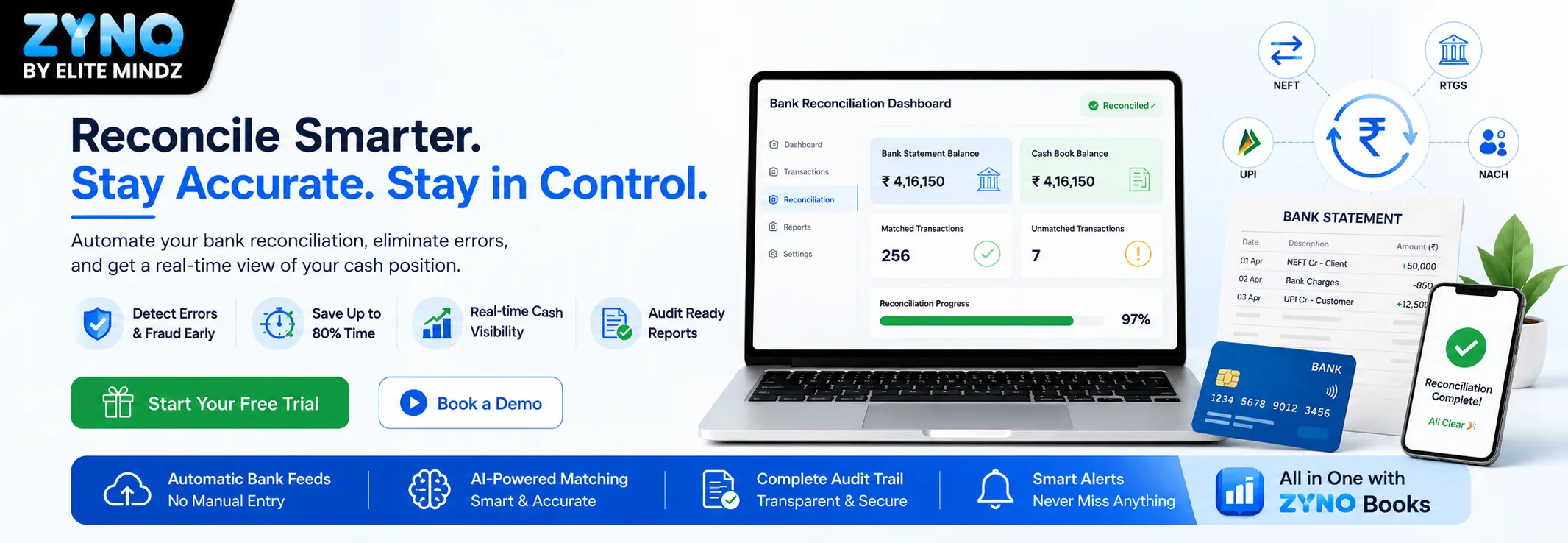

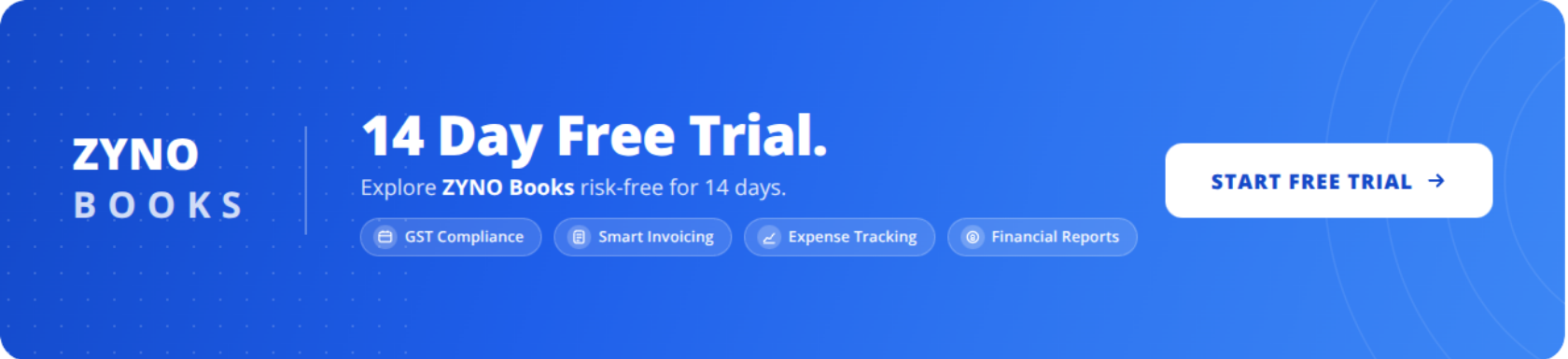

The Ultimate Guide to Managing Your Business with ZYNO Books

Read More →- ZYNO AI

-

AI Agent Development

-

AI Chatbot Development

-

AI Consulting

-

AI OCR

-

GAI Consulting

-

GAI Development

-

Machine Learning

-

Computer Vision

-

Low Code / No Code Services

-

Hire A Developer Services

-

AI Development

.webp)

.webp)

.jpg)

.jpg)

.webp)

.webp)

Meaning,FullForm,Format&Examples.webp)

.webp)

.webp)

.webp)

.webp)

(1).webp)

.webp)